Microsoft’s Gaming Problem, And The Downsides Of AI

If you’re a Patch Notes person, or you prefer Substack, I got you covered here: https://substack.com/@patchnotesgaming

Alright, two quick personal notes before we get into it.

First, I’ll be at D.I.C.E. Summit in Las Vegas, February 10–12. My calendar is nearly full, but if you want to catch up, talk Patch Notes, talk attention economics, grab a coffee, grab a drink, or play a little craps, let me know, I’ll make room for smart conversations. Here is my Calendly.

And if you want something more casual, Greg is hosting a Player Driven event during DICE, and I’ll be there too. Details below,

When: Feb 10 @ 4PM PST

Where: Aria Sky Suites, Las Vegas

Second, believe it or not, I’m one person, and I do most of this myself, so there is a real chance Patch Notes pauses next week while I recover from DICE and catch up on everything I missed while I was running around Vegas. We’ll see what happens in the news, if the week demands a post, I’ll find a way, if not, I’ll be back the week after with something worth your time.

Third, I’ll also be at GDC in San Francisco, March 9–13. If you want to grab coffee there, tell me, I’ll start locking meetings as soon as I get back from DICE. But if you want to get on my radar now, here is my Calendly.

As I thought about this week, two things kept circling back in my head. The first was Google’s Genie 3 and the wave of “this changes everything” takes that followed. The second was Microsoft’s Q4 earnings, and the Xbox miss. To me, it says more about corporate incentives, and where this could be going, than it does about a single quarter. Those two stories are connected, even if it doesn’t look like it at first glance.

Before we touch the numbers, I want to start with a quote from mindGAME Data founder Brian Rogers, because he nailed the part of the Genie 3 discourse that’s been driving me crazy.

I’ve seen an insane number of posts about Google Genie 3 and how this is “the future of games.” That reaction tells me one thing very clearly: a lot of people have never actually shipped, marketed, or sustained a real game.

Remember Google Stadia? Infinite resources, elite engineers, zero understanding of why people buy and play games. Spectacular failure. Games are not: 60 seconds of vibes... A tech demo... A random video loop

Games are systems. They’re balance, progression, retention, community, trust, live ops, art, psychology, platform politics, and years of iteration. They’re built by teams who deeply understand players, not by investors watching a flashy clip and declaring disruption.

Every time Wall Street applauds this stuff, it quietly reinforces the idea that games are “easy” and replaceable which is how you justify laying off the very people who actually know how to make them. If you’re pumping out ‘game developers are toast’ posts and you work in this industry, you are actively rooting for our colleagues to be fired and replaced with a pipe dream.

AI is/will be a powerful tool in game development. It will not replace game developers. And it definitely won’t replace taste, craft, or player understanding. If a 60-second generated video were enough, the industry would’ve collapsed a decade ago. But it didn’t.

I agree with Brian, games are closer to social networks than most people want to admit, and the stickiness is not only the map and the mechanics. It’s the shared language, the shared meta, the shared memories, the group chats, the Discord servers, the communities, the Twitch streams, the LAN parties, the clans that have existed in World of Warcraft for decades.

A one-for-one generated open world might be interesting to watch in a loop, but it’s not the same thing as a reason to engage and stay. Players can sniff out sterile, boring, “this was made by nobody” experiences fast, they always have, and that’s probably part of why the broader player community has been so allergic to AI hype in the first place.

That said, I’m also not in the “AI has no use” camp, not even close. I think Brian has it right, AI can be a powerful tool, and we’re already seeing that play out in everyday life.

This week my son started spring baseball, first practice, third year with the team. The league handed the coaches a new net, no one could figure out how to assemble it, and the coaches were juggling a hundred other things at once.

I volunteered, stared at the pile of parts for a moment, and realized I was wasting time. Five years ago I would have bounced between noticing the brand, googling it, getting buried in ads, and maybe landing on a YouTube video that might or might not match the exact model.

Instead, I took a picture of the logo and the parts, asked ChatGPT what it was, and it surfaced the PDF manual. Two minutes later the net was up, practice kept moving, and I got to pretend like I knew what I was doing. That’s the version of AI I believe in, a better hammer, or maybe a better analogy is the horseless carriage.

In the 1700s, nearly 80% of Americans were farmers. By the 1900s that was closer to 40%. Today it’s around 2%. We didn’t “replace” people, we replaced tools, and we kept moving.

AI feels like that to me. The question isn’t whether the carriage exists, it’s whether we’re the horse… or the person riding it, I’m firmly in the rider camp.

Now here’s where Microsoft comes in. When the market freaked out about Genie 3, I saw the usual “games are over” panic. Full disclosure, I joked “buy the dip,” and I actually did, shout out to Take-Two Interactive. I’m not going to turn this into a Grand Theft Auto VI thesis, but I do think a lot of the “AI just killed game companies” reaction is nonsense. Tools are not entertainment experiences, and tech demos are not games.

The real risk, the one that matters for the industry, is that AI is turning the biggest companies in the world into capital allocation machines with a single obsession, compute. The market is judging their success and failure on whether they can spend billions fast enough, justify it fast enough, and secure supply they don’t control. If you are a gaming business sitting inside that machine, you feel it, even if your quarter is fine.

Which brings us to the earnings, and my immediate reaction to the Xbox miss wasn’t “got them,” it was, this was unsurprising. We’ve been writing about this for months.

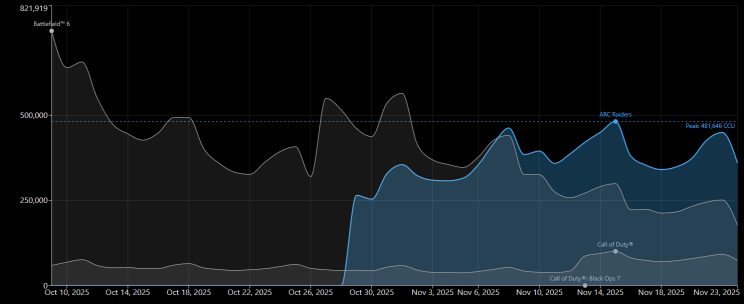

We wrote about Call of Duty versus Battlefield 6, and what stood out wasn’t some hot take, it was how clearly the signals were diverging. The announcement and follow-up marketing beats for Call of Duty: Black Ops 7 were not matching Battlefield 6 levels, and they weren’t even matching Arc Raiders in the same window, which is exactly what we were saying at the time. So when it became clear the quarter missed, we were basically unsurprised, surprised it got to that point, but not surprised by the outcome.

We also knew Ninja Gaiden 4 wasn’t going to be a needle-mover. You could see it early, from the Xbox Showcase beats in early 2025 through the rest of the year, it just never started trending like the titles it needed to compete with in Q3 and Q4, and it wasn’t even in the same universe as adjacent comps like Ghost of Yōtei.

And we knew The Outer Worlds 2 wasn’t tracking like a breakout, it wasn’t even tracking anywhere near The Outer Worlds 1. It also took the prestigious “post-Showcase highlight” slot coming out of Summer Game Fest, the same kind of spotlight Call of Duty: Black Ops 6 benefited from the year before. Watching it in real time, you could tell it wasn’t moving the needle.

Instead of re-litigating Game Pass again, I want to zoom out. After reading the Xbox numbers, then reading the broader Microsoft earnings context and the analysis around it, I wanted to take a more macro look.

What is Xbox Gaming as a portfolio, what does it actually own, what is working, what isn’t, and what does it mean to be a massive gaming business inside a parent company that is being judged in a different market entirely.

Let’s dig in.

Microsoft Gaming - The Berkshire Hathaway Of Gaming

Three Chunks, One Holding Company

When most people say “Xbox,” they still picture a console. On Microsoft’s org chart, though, all of this sits inside Microsoft Gaming, led by Phil Spencer, and it’s built more like a holding company than a single publisher.

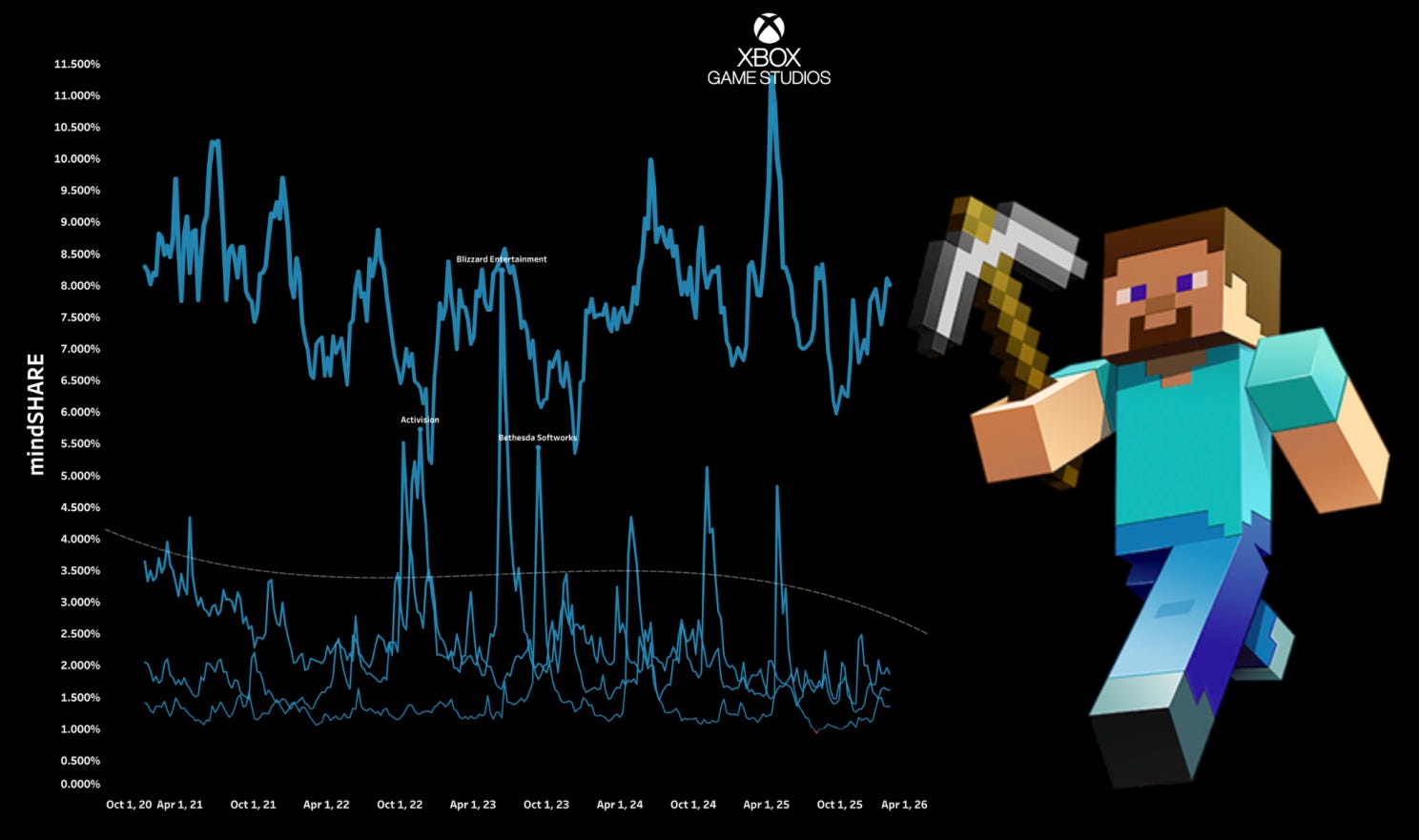

Under that umbrella there are three main chunks. Xbox Game Studios Publishing is the first-party label, the part of the portfolio that includes Minecraft, Halo, Forza, Sea of Thieves, Age of Empires, Flight Simulator, and the rest of the internal slate. ZeniMax Media is the Bethesda Softworks side of the house. When it hits, it hits big, but those releases do not come out all that often, so the baseline tends to hover much lower between major moments. And then there is Activision Blizzard King (ABK), the blockbuster console and PC machine plus the mobile engine, where Call of Duty and Candy Crush live under the same roof.

If you look at the portfolio through mindGAME Data, the scale is real. Xbox Game Studios tends to hover around 7–8% of total gaming attention, ABK contributes roughly 4–4.5% combined, and Bethesda sits around 1% outside major release windows.

But there’s a catch, and it explains why Microsoft’s strategy keeps rhyming. That 7–8% Xbox Game Studios number is almost entirely Minecraft, and Minecraft alone is roughly 7% of the entire market in our read, which leaves everything else fighting over the remaining half point to a point.

As someone who grew up on Xbox, especially in my formative college years, that’s still a weird sentence to write. My gamertag was Girls Hockey, I have way too many fond memories of Bungie-era Halo, especially Halo 1 in dorm-room LAN parties, and I co-op’d my way through the major Gears releases. Which is why it still feels strange to admit it, without Minecraft, Xbox Game Studios is structurally pretty thin.

On the revenue side, this portfolio is a multi-billion-dollar business. Microsoft does not give the clean breakout everyone wants, but it does disclose quarterly gaming deltas, and you can back into the rough size from there. In Microsoft’s fiscal year 2026 Q2 (the quarter ended December 31, 2025), Microsoft said gaming revenue decreased $623M, or 9%, which implies a roughly $6.3B quarter, down from about $6.9B a year ago. Over the last couple years it has generally landed in the $5–7B per quarter range, depending on the comp and the mix.

That’s the frame that matters for the rest of this piece. Microsoft Gaming is a big business in absolute terms, but it lives inside a parent company that is increasingly optimized around cloud, AI, and capital allocation. In that environment, “Xbox” stops being primarily about selling boxes and starts being about distribution across devices, an endpoint strategy.

That shift is rational, but it also creates a new kind of tension. You can ship a great game and still struggle to matter to the parent org in the way a great cloud quarter can, which is exactly why the acquisition story and the attention story keep looping back into each other.

Xbox is becoming a distribution layer across devices, not a box-first ecosystem. To keep that model fed, Microsoft needs more content than Xbox Game Studios can reliably produce on its own, which is why the company has leaned so hard into acquisitions.

Buying Gravity

So when you look back at the last decade, the playbook becomes obvious. When the internal slate can’t carry the strategy on its own, Microsoft buys more gravity, and the “why” is usually some variation of grow the audience, grow the library, grow the reach.

From a CNET interview after the ZeniMax deal was announced, Satya Nadella said it directly,

“You can’t wake up one day and say, ‘Let me build a game studio… The idea of having content is so we can reach larger communities.’”

Satya Nadella, CEO, Microsoft, CNET, Sept. 21, 2020.

You can read the acquisition announcements the same way. Mojang was $2.5B in 2014, ZeniMax was $7.5B in 2020, and ABK was $68.7B announced in 2022 and closed in 2023. The language differs, but the through line is consistent.

“Minecraft is more than a great game franchise – it is an open world platform, driven by a vibrant community we care deeply about.”

Satya Nadella, CEO, Microsoft, Reuters, Sept. 15, 2014.

“Quality differentiated content is the engine behind the growth and value of Xbox Game Pass.”

Satya Nadella, CEO, Microsoft, Microsoft News Center, Sept. 21, 2020.

“This acquisition will accelerate the growth in Microsoft’s gaming business across mobile, PC, console and cloud.”

Microsoft, statement, Microsoft News Center, Jan. 18, 2022.

That’s the move. In a power-law attention market, one of the clearest paths to staying dominant is to buy your way out of whatever position you’re drifting into, and Microsoft has the balance sheet to do it. The harder question is whether this is a healthy long-term posture, when each spending spree gets more expensive and “grow” increasingly means “buy.”

To explain the conundrum Microsoft is in, I want to start with the acquisition that’s been quietly compounding for more than a decade. I’ll reference ABK and Bethesda when it helps, but the first big modern purchase that shows both the upside and the problem is Minecraft.

The Good, Minecraft Prints, And 2026 Has Real Upside

The Quiet Giant

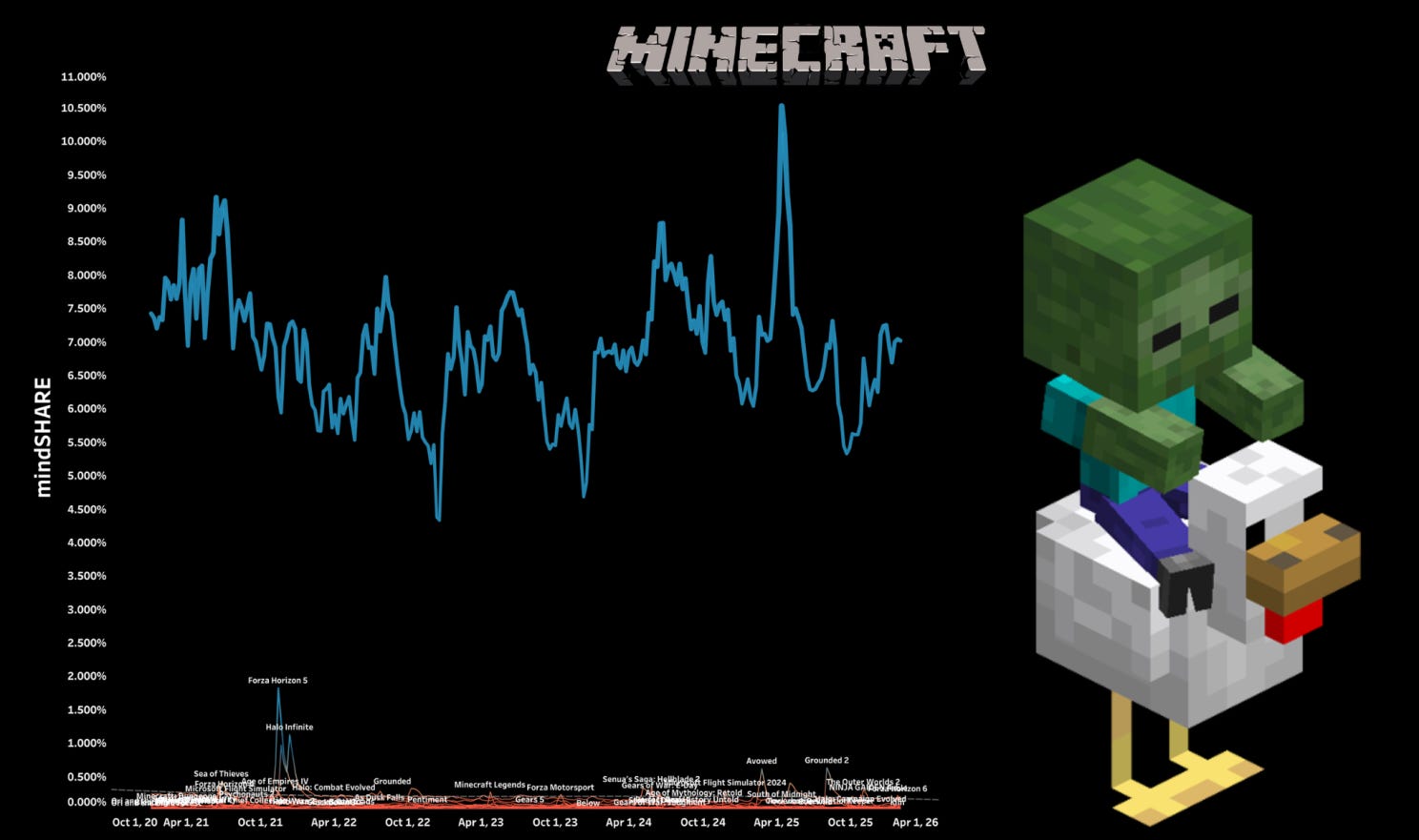

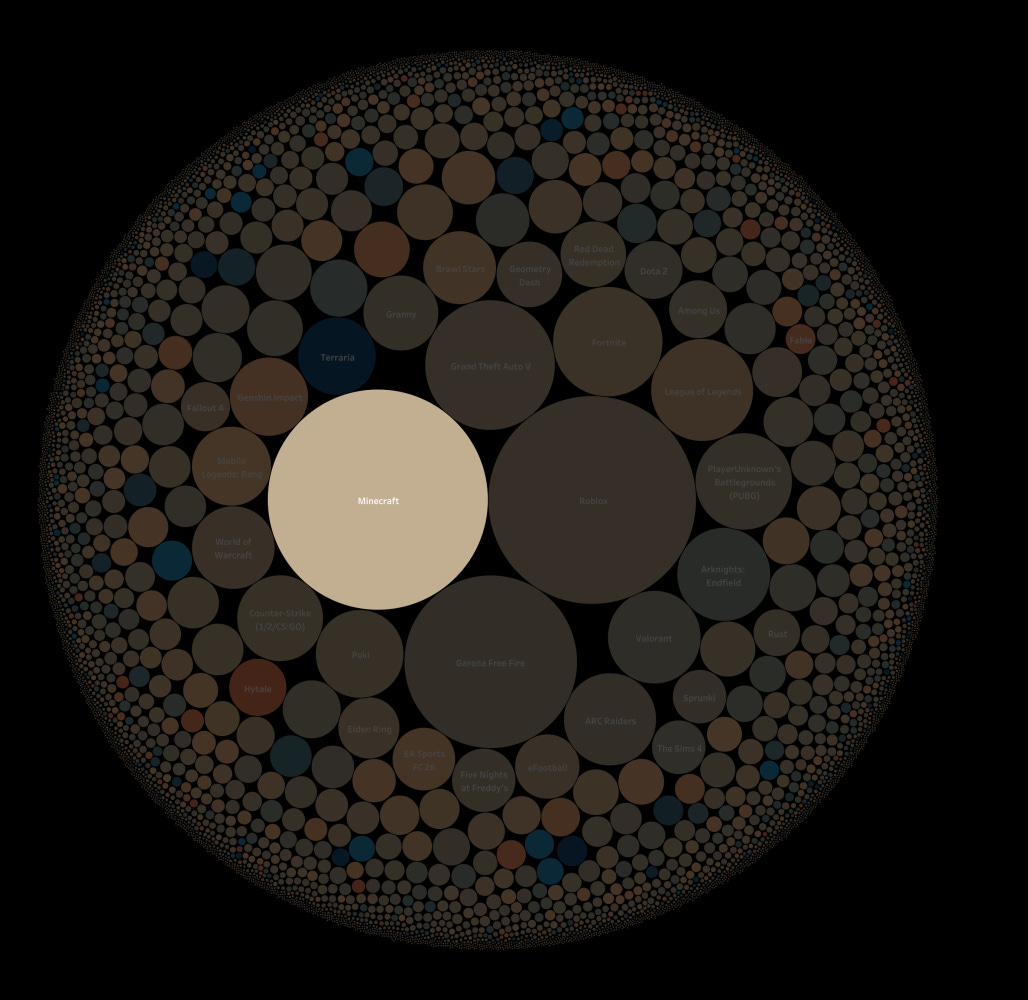

If you want the simplest possible way to understand why Microsoft Gaming is “big,” start here: in mindGAME Data, Minecraft is the portfolio, and its only real peer in absolute attention is Roblox. Since 2020 those two have basically traded the #1 and #2 spot, and then there’s a cliff.

At the low end, Minecraft still sits around ~6% mindSHARE. At its peak it hit ~10.5%, and if you’ve been watching the last few years of signal behavior, you already know what that kind of spike usually means, the IP just crossed into a broader cultural moment.

The distribution of the signals tells the same story. Minecraft can do north of 45M searches a week, it’s effectively #1 on YouTube in most weeks, and it lives in the top tier of Twitch, usually hovering in the 8–12 range. Even on TikTok, where Roblox has the bigger gravitational pull, Minecraft still sits at absurd scale, more than 850B lifetime views.

If you want the “why,” it’s not complicated. Minecraft turns play into identity. It behaves more like a social network than a product SKU, and it has the same compounding flywheel the biggest platforms have, creators make things, communities remix them, and the base game stays relevant because the community keeps rebuilding it.

What’s underappreciated is that this is not just a Western phenomenon, Minecraft is massive in China too, and it got there the hard way, by partnering locally and adapting to the market. In 2016, Microsoft, Mojang, and NetEase announced a five-year exclusive licensing agreement to bring Minecraft to mainland China on mobile and PC, with Mojang developing a version tailored for the Chinese market.

“We’ll always embrace opportunities to bring Minecraft to new players around the world, widening our community, and giving us a new perspective on our game.”

Jonas Mårtensson, CEO, Mojang, PR Newswire, May 20, 2016.

“We are excited to bring Minecraft to Chinese audiences, and expect our large online community to embrace this preeminent game.”

William Ding, CEO and founder, NetEase, PR Newswire, May 20, 2016.

That partnership turned into a real platform, and at the 2023 Minecraft Developer Conference, the China Edition team shared that registered users had reached 700 million. That number is hard to wrap your head around even by “China numbers,” and it helps explain why Minecraft is one of the very few game ecosystems that can trade the top spot with Roblox over multi-year stretches.

Then there’s the part that’s hard to ignore if you’ve spent any time around brand licensing. Minecraft isn’t just a game anymore. It has been a long-running LEGO line for more than a decade, it has a modern film footprint, and it’s one of the rare examples of a game IP that feels culturally evergreen rather than seasonally hot.

Which is why I keep coming back to the strangest corporate reality in games, Microsoft owns the biggest game in its portfolio, and it almost never treats it like a headline.

Yes, Minecraft shows up in earnings materials, but it usually shows up as one sentence inside a longer paragraph about “gaming,” and Microsoft almost never breaks out the actual numbers.

“Minecraft saw record monthly active usage and revenue this quarter, thanks in large part to the success of the Minecraft movie.”

Satya Nadella, CEO, Microsoft, Microsoft FY25 Q4 earnings call, July 30, 2025.

That’s a pretty incredible line to bury. If Meta owned Roblox, you would hear about it every quarter. If Disney owned Epic, you’d hear about it every quarter. If TikTok owned Grand Theft Auto, it would be on stage at every keynote.

Microsoft owns Minecraft, and most of the time it gets treated like plumbing.

That’s the “quiet giant” point. This is the acquisition that worked so well it became invisible, and it’s the single biggest reason Xbox Game Studios looks bigger than it is.

Two Shots On Goal For 2026

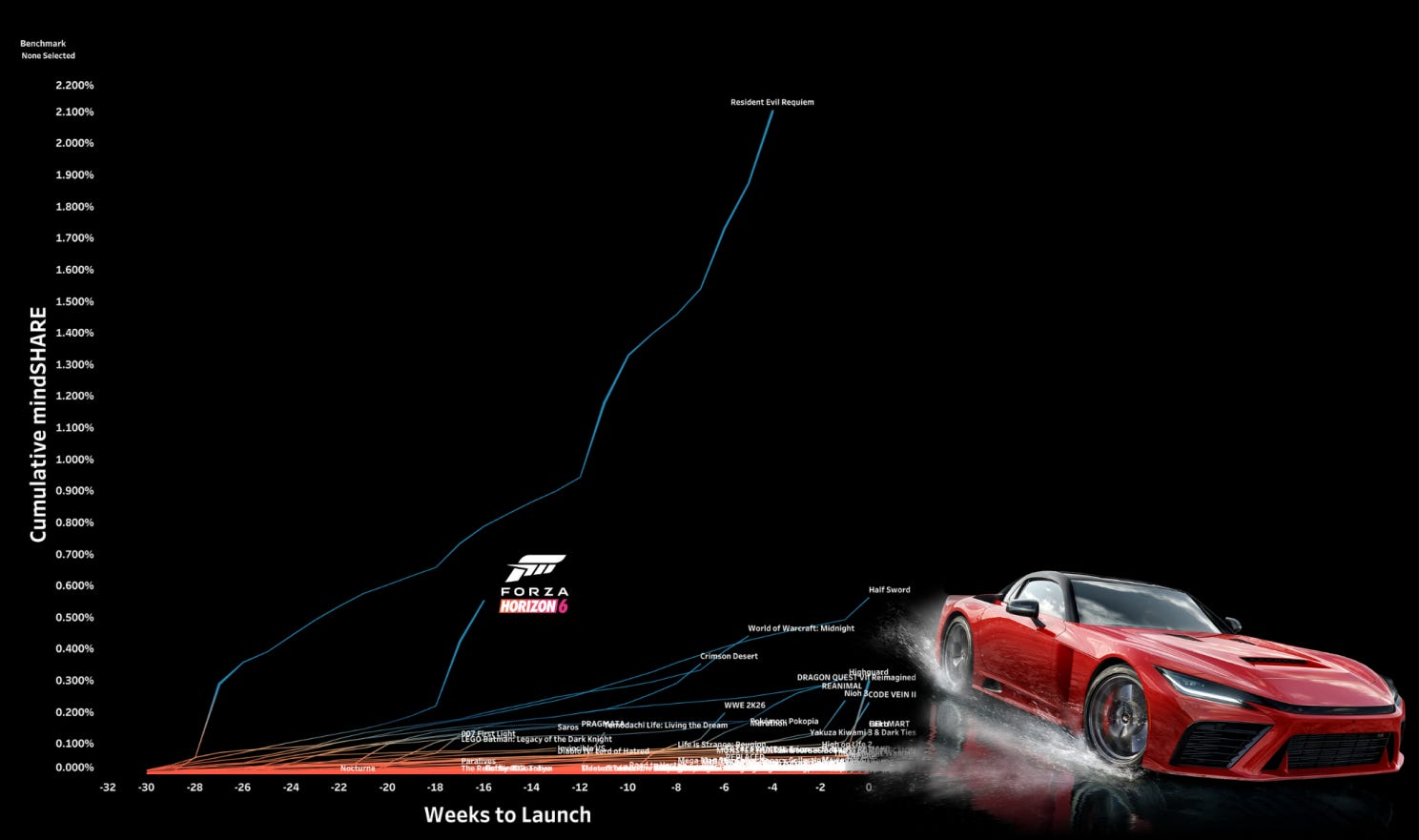

To be fair, though, that doesn’t mean Xbox Game Studios has no upside outside of Minecraft. Looking ahead, there are two real shots on goal this year, Forza Horizon 6 and Fable, and they matter because they test a simple question, can Xbox still ship tentpoles that feel like events.

In our tracker, Forza Horizon 6 is already sitting around ~0.55% cumulative mindSHARE more than 15 weeks from launch. Right now it looks like the clear second-biggest game in the first half of the year behind Resident Evil Requiem, and on our internal scorecard it’s flirting with a borderline S-tier trajectory.

Fable is the other candidate. The caveat is release timing, if it ends up crowded into a fall window with Grand Theft Auto VI, that is a different fight. But even with an unknown date, it’s already sitting around a 0.379% cumulative mindSHARE score, which makes it the second-biggest unreleased Xbox Game Studios title in our system right now, in roughly the same neighborhood as Tomb Raider: Legacy of Atlantis.

And this is where the “quiet giant” point becomes more than a fun observation. If Minecraft is so massive that Microsoft barely needs to talk about it, how big do Forza and Fable need to be to matter to Microsoft, the larger parent org, and the corporate narrative that actually moves the stock. Can they actually move the needle, or do they simply prove Xbox can still ship real tentpoles while Wall Street’s attention is elsewhere.

The Bad, Not Just A Quarter

The Miss

Before we get into the weeds on any one release, it’s worth zooming out. Microsoft Gaming is a big business, and on a pure revenue chart it has been moving in the right direction, just not in a smooth line.

The growth has come in step-functions, and those step-functions line up with acquisitions. Pre-Bethesda, gaming revenue in FY2020 was $11.6B. Post-Bethesda, FY2021 jumped to $15.4B. Then it basically hovered in the mid-teens through FY2022 and FY2023.

Then ABK arrived. FY2024 stepped up to $21.5B, with roughly nine months of ABK in the mix, and FY2025 reached $23.5B on a full year. That is a real growth story.

The catch is that “revenue up” does not automatically translate to “corporate priority up,” especially inside a parent company whose other businesses are on a tear and whose attention is pulled toward higher-margin engines. In that kind of environment, it’s hard to get noticed when you’re up, and it’s harsher when you’re down.

Which brings us back to the quarter.

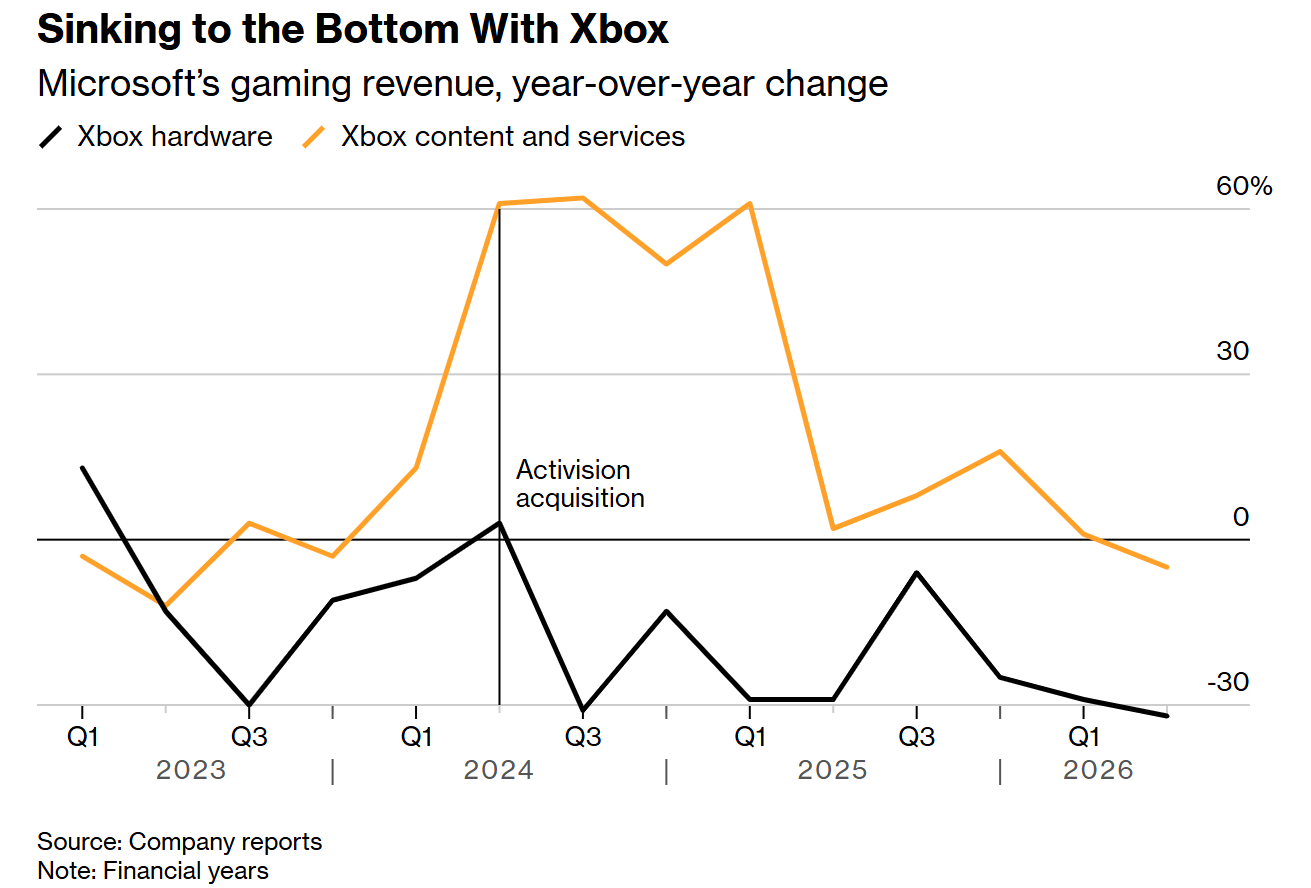

Microsoft said gaming revenue declined 9%, hardware fell 32%, and Xbox content and services declined 5%. That is a rough combination, especially in a holiday quarter, and it also reads like the box is shrinking faster than the rest of the ecosystem can compensate for.

If you’ve been reading Patch Notes, the miss shouldn’t feel mysterious. In our signals, Call of Duty: Black Ops 7 never built the same pull as prior years. At launch, Black Ops 7 peaked at roughly 1.07% mindSHARE versus Black Ops 6 at 3.71% the year prior, a ~71% decline, and the weakest mainline Call of Duty launch peak we’ve seen since 2019.

That’s still enormous by normal shooter standards. But when the biggest franchise in your portfolio is expected to carry a holiday quarter, “soft” turns into “miss” fast.

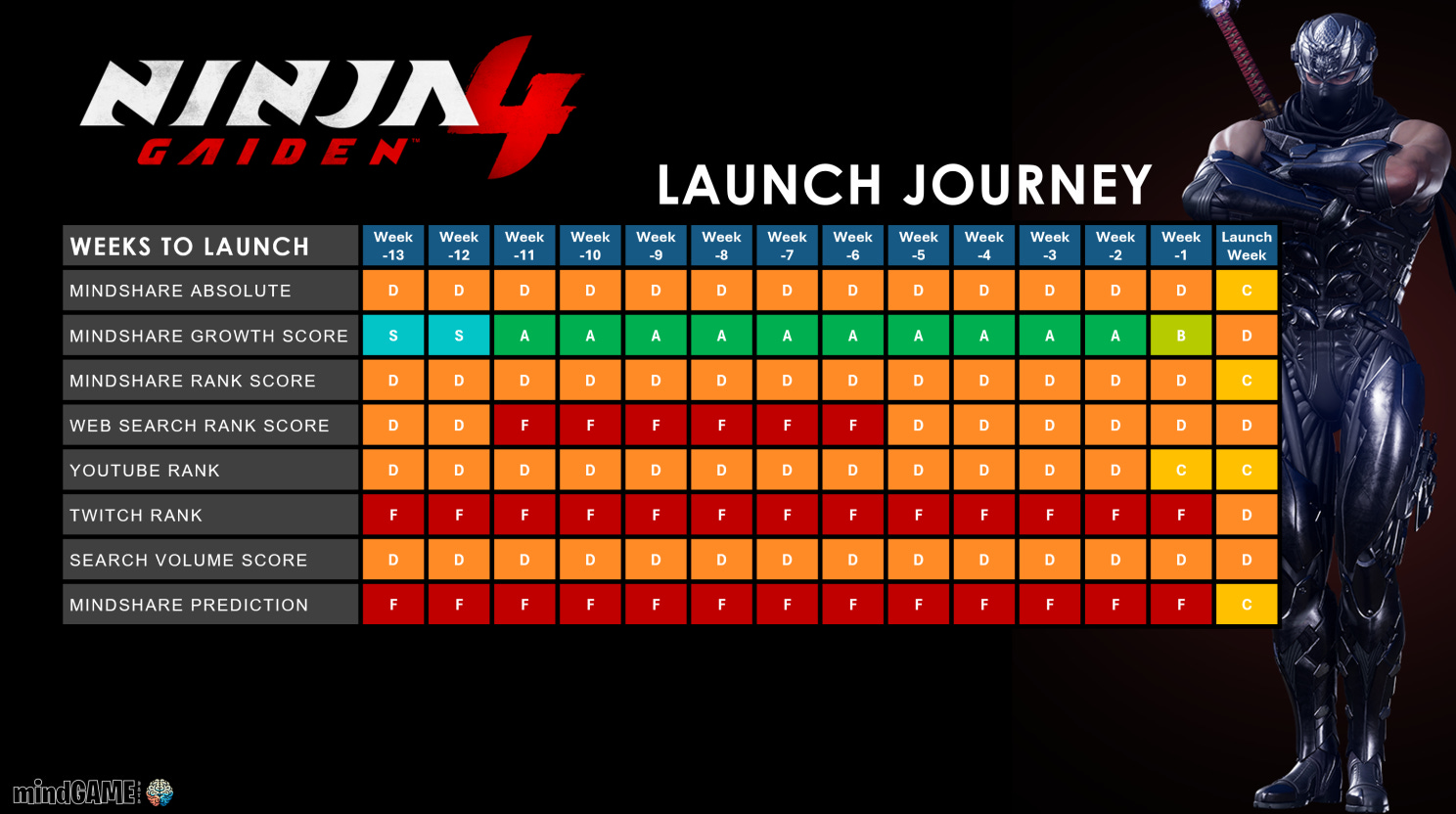

It also wasn’t only Call of Duty. Microsoft needed the rest of the slate to feel like real events, and by every public signal we track, Ninja Gaiden 4 did not land. Cumulative mindSHARE at launch was 0.45%, and its channel ranks never cracked the top 25, Search #76 (around 750k queries), YouTube #66, Twitch #41, with roughly 35M lifetime views on TikTok. Steam CCU peaked around 11,000 on release, then fell off a cliff.

And then there’s The Outer Worlds 2, which is the kind of miss that hurts because it’s supposed to be part of the “Xbox can still ship a flagship RPG that actually moves the needle” story. At launch it ranked #32 in Search, #86 in Video, and #35 in Streaming, with cumulative mindSHARE at 0.599%. For context, Grounded 2, a much smaller game on paper, and presumably on a much smaller budget, hit 1.077% cumulative mindSHARE.

That gap is the point. It’s not that these teams can’t make good games, it’s that the portfolio needs dependable, repeatable, multi-channel demand, and too many of the big beats are landing below where they need to.

This is also where the “bad” story turns into a pressure story.

The Pressure

A Bloomberg Businessweek profile of Obsidian captured the tone, because it puts real people behind the spreadsheet. Obsidian shipped three games in 2025, which is a rare feat for a studio of its size, but internally it was messy, stretched support teams, strained resources, and two of those games missed Microsoft’s sales forecasts.

Sawyer’s point is that the “Year of Obsidian” headline is slick marketing, but it is also a warning label. When releases stack up like that, it usually means something went sideways upstream.

“Spacing those releases helps the company manage its resources and not burn everybody out… It’s not good to release three games in the same year. It’s the result of things going wrong.”

Josh Sawyer, Studio Design Director, Obsidian Entertainment, Bloomberg Businessweek, Feb. 3, 2026.

Urquhart doesn’t describe the misses like a crisis, but he does frame them the way a leader has to frame them inside a bigger machine, what did we learn, and what do we change. That’s where budget, timeline, and expectations start to collide.

“They’re not disasters… It was more like: ‘That sucks. What are we learning?’”

Feargus Urquhart, Studio Head, Obsidian Entertainment, Bloomberg Businessweek, Feb. 3, 2026.

The “learning” sounds boring until you remember what it implies. It’s not just “ship faster,” it’s “stop spending effort where players won’t feel it,” and that’s a brutal thing to say out loud when you’ve already sunk years into a project.

“Do people really care that we spent an extra hundred person-months on the inventory screen?”

Feargus Urquhart, Studio Head, Obsidian Entertainment, Bloomberg Businessweek, Feb. 3, 2026.

Then you get the operational tell, Obsidian is leaning into reuse and outsourcing, and it’s making hard calls earlier. Parker’s line is basically, if we were doing this purely internally, we’d keep sanding the edges for months, but the economics don’t reward that anymore.

“If this was one of our internal teams, we would work on this for another two or three months.”

Chris Parker, Obsidian co-founder, Bloomberg Businessweek, Feb. 3, 2026.

And above all of that is the mandate. Microsoft’s public framing is still supportive, but it also reveals what the portfolio is being optimized for, reach more players, reach them faster, and do it with a machine that can scale.

“Obsidian develops games that are central to our vision of reaching more players than ever before.”

Mary McGuane, General Manager, Xbox Game Studios, Bloomberg Businessweek, Feb. 3, 2026.

If you combine that “reach more players” mandate with the reported push for much higher profit targets, it’s easy to see why the pressure feels so acute. Bloomberg has reported an across-the-board goal of 30% profit margins at Microsoft’s Xbox gaming division. For context, The Verge cited the industry average as roughly 17–22% when summarizing the report. (Bloomberg, Oct. 23, 2025; The Verge, Oct. 23, 2025.)

And that is where this stops being a “what went wrong this quarter” conversation and starts being a “what is Xbox inside Microsoft” conversation.

The Ugly, A Rounding Error In A Mega Conglomerate

How It Feels Inside Microsoft

Here’s the ugly part. Microsoft Gaming can be a $23B a year business and still feel like a rounding error inside Microsoft, because the parent company is operating at a scale where the gaming swings don’t really change the story.

In the holiday quarter, Microsoft printed $81.3B in revenue and $38.5B in net income. That is an absurd amount of money, and it’s why the company’s real anxiety is not “did Xbox have a good quarter,” it’s “are our biggest engines compounding the way Wall Street expects.”

On that scale, gaming revenue landing in the $5–7B per quarter range is both massive and oddly easy to shrug at. Outside of Microsoft, a $6B quarter is the kind of business that gets written about like a phenomenon. Inside Microsoft, it can feel like a side quest, and that incentive mismatch shows up everywhere.

Brad Sams, who covers Microsoft extensively, did a great earnings-reaction video worth a listen.. if this is your sort of thing. His core point is simple, Xbox can be large in absolute terms and still become a smaller slice of a much faster-growing company.

Brad also makes two other points that are worth holding in your head. First, Brad’s point is that Xbox is one of the few places Microsoft still touches consumers emotionally, a real consumer brand inside a company dominated by enterprise workflows, even if I’d argue that bond has weakened over the last decade. Second, the longer the parent company is forced to think in terms of opportunity cost and capital allocation, the more Xbox has to justify not just its quarterly results, but its reason for being inside this specific portfolio.

That’s the tension. Gaming is strategically valuable as a consumer touchpoint, but it is strategically awkward as a business unit inside a company optimized for software-like economics.

You can feel it in the way Xbox has been run over the last decade. If the internal slate can’t manufacture enough gravity, Microsoft buys it. As box sales slow, the strategy shifts toward distribution to maximize reach, and the recent wave of day‑one PlayStation releases is the clearest tell. A missed quarter then translates into the familiar pressure, “ship faster, reuse more, spend less,” leaving teams overworked, cutting scope, and chasing margin targets that feel unrealistic for how games actually get made.

This is also why the succession chatter lands at all, even if it’s mostly speculation. The question isn’t whether Satya Nadella will wake up tomorrow and kill Xbox. The question is what happens in a future Microsoft leadership regime, especially a finance-led one, when gaming keeps requiring massive checks, occasional regulatory wars, and constant reinvestment… and the upside still doesn’t move the parent company’s narrative the way AI and cloud do.

Brad even floats the extreme version of that thought experiment, a future where Xbox is restructured or spun out in some capacity under different leadership.

You don’t have to agree with the prediction to take the underlying point seriously. Inside Microsoft, gaming is being compared to businesses that scale with near-zero marginal cost, and it’s being compared to an AI buildout that is now absorbing executive attention, capex, and narrative oxygen.

After ChatGPT, The Math Changes

Which is why the timing matters. Something shifted when ChatGPT hit the mainstream. Microsoft didn’t just “get excited about AI,” it got pulled into an arms race where compute is destiny, and everything else becomes a question of opportunity cost.

That’s the ugly. Xbox can win in gaming and still struggle to matter inside the parent company, especially when the parent company is sprinting toward an AI future.

And that brings us back to Genie 3, because the scary part of AI isn’t a tech demo making a weird sandbox, it’s the capital and compute gravity that can squeeze every other part of the portfolio.

The AI Of It All, Or: How I Learned To Stop Worrying And Love The CapEx

Genie 3 Is A Distraction

The real AI panic isn’t Genie 3.

Genie 3 is a flashy demo that makes for great discourse, it’s easy to watch, easy to fear, and easy to turn into a “games are over” narrative. The weirder part is that Wall Street treated it like a real product moment.

When Google unveiled Project Genie, video game stocks sold off hard. Take-Two dropped roughly 8–10% on the day, Roblox was down roughly 12–13%, and Unity got smoked, down roughly 21–24%. That dip didn’t magically disappear the next morning either, by the time Strauss Zelnick was asked about it, Take-Two was down about 12% from the prior Friday.

This is why I joked “buy the dip,” and why I’m generally bullish on games surviving the AI hype cycle. Games are social networks, the big categories are calcified, and network effects do not unwind overnight. People are talking about disruption like it’s a light switch, but social gravity doesn’t work that way.

Zelnick’s response was basically the more obvious point, and it’s the right one. Project Genie is a tool, not an entertainment experience.

“Tools are not entertainment experiences. Creators use tools to create great entertainment.”

Strauss Zelnick, CEO, Take-Two Interactive, The Game Business, Feb. 4, 2026.

That is the correct mental model. AI is a hammer, and in games we’re still the carpenter, or if you prefer the earlier analogy, AI is the carriage and creators are the riders, the tool moves faster, but it still needs someone steering it.

The real risk is what the hammer is doing to the companies holding it.

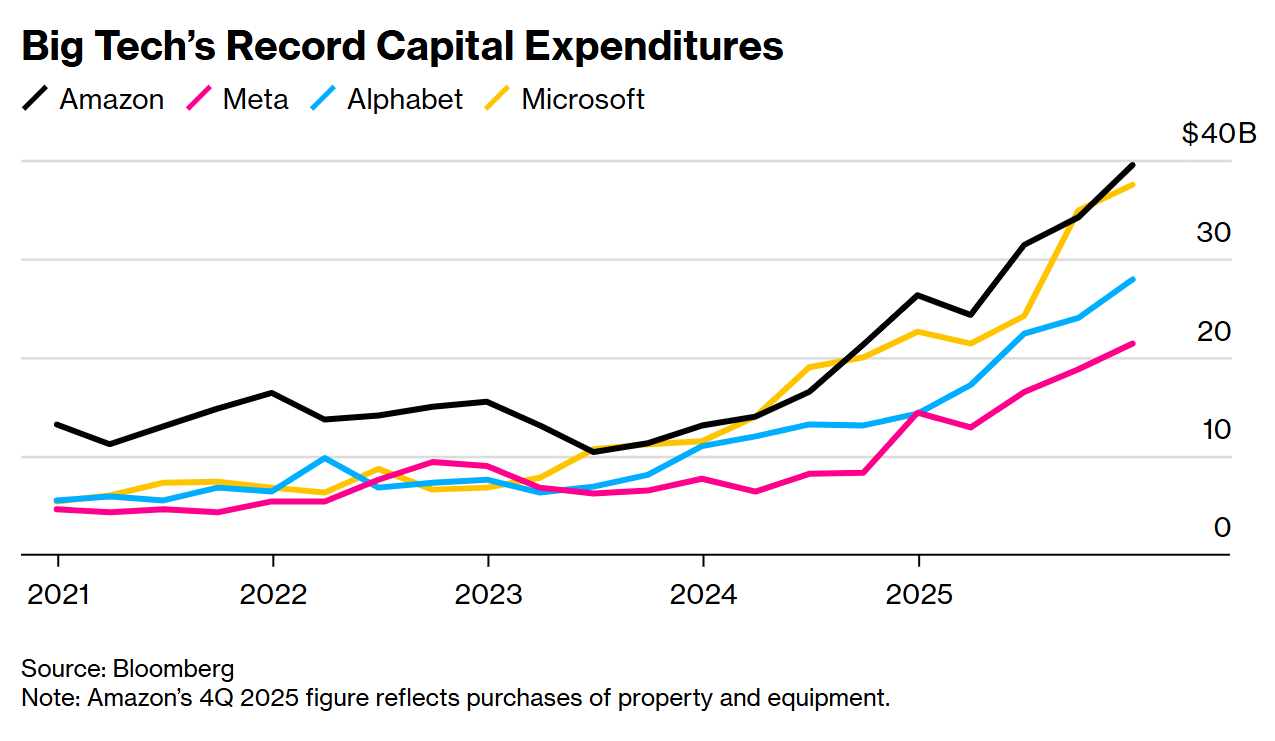

Microsoft spent $37.5B on capex in the holiday quarter, up 66%, because compute is now the constraint and the obsession. At the same time, Microsoft disclosed commercial remaining performance obligations of $625B, up 110%, and OpenAI represents roughly 45% of that backlog.

That combination is the new gravity.

It creates two paths that both lead to the same place for gaming.

The first path is the bubble story. If the demand is softer than the contracts imply, if OpenAI stumbles, restructures again, or simply can’t convert commitments into real cash at the pace everyone expects, then the pressure snaps back onto Microsoft. Not “some pressure,” real pressure, the kind that forces portfolio triage.

And if Microsoft needs to save what it can and cut what it must, gaming is exposed, not because it’s small, but because it’s expensive, cyclical, and harder to explain to a board that is trying to win an AI arms race. In that world, Game Pass checks shrink, big content swings get harder to justify, and “why do we still own this” stops being a Reddit argument and becomes an internal question.

The second path is the opposite, the demand is real, OpenAI doesn’t crater, and the AI race simply keeps accelerating. That’s not “good news” for gaming either, because it means the capex machine has to keep eating. The price of GPUs, memory, networking, power, all of it rises, and the competition is not Sony or Nintendo, it’s Amazon, Google, Meta, and whoever else is willing to write the next $50B check.

TSMC, The Chokepoint

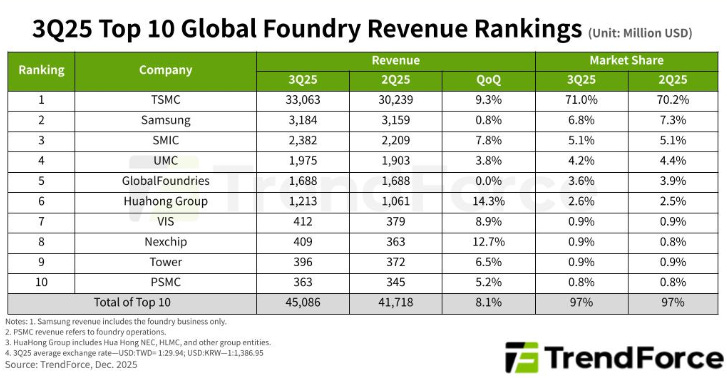

To understand why this matters, it helps to name the chokepoint: TSMC.

TSMC, Taiwan Semiconductor Manufacturing Company, is the dominant advanced-chip foundry, the factory floor behind the silicon designed by Nvidia, Apple, AMD, and a huge chunk of the modern AI stack. In practice it’s a global bottleneck, and bottlenecks eventually turn into price.

This is where Ben Thompson’s Stratechery framing is useful, not because of the “AI kills games” narrative, but because of the supply chain math.

In his piece on TSMC risk, Thompson’s point is that the real bottleneck is silicon. Hyperscalers can commit capital all day, but if TSMC can’t add capacity fast enough, scarcity persists, and scarcity turns into price.

That’s the nasty loop. If demand stays hot, Microsoft has to keep writing bigger checks for GPUs, memory, networking, and power. If supply stays tight, guidance misses get punished harder, and the easiest way to protect the core story is to squeeze anything that isn’t core.

In a Microsoft context, “not core” is rarely Azure, it’s everything downstream that competes for capital. Gaming can be a great business and still end up at the end of the duck-duck-goose line, not because it’s failing, but because it’s the most optional at the exact moment the market is least forgiving.

Until there is a real second source of leading-edge capacity at scale, whether Intel, Samsung, or someone else, we’re basically stuck with TSMC as the choke point, and “scarcity becomes price” stays the law of the land.

That’s why I keep saying Genie 3 is a distraction.

The fear is not that AI will replace game developers overnight. The fear is that the AI arms race, whether it booms or busts, forces Big Tech companies into a posture where everything becomes opportunity cost, and gaming is an easy place to squeeze.

Which brings us to what this means for the broader industry, because Microsoft doesn’t just affect itself. It affects everyone else it funds, subsidizes, and pulls into its gravity.

The Industry-Wide Risk

The Subsidy Layer

Despite my critiques of Game Pass, I don’t think people fully appreciate how much Microsoft has become a funding and distribution layer for the industry. The service can be value destructive in the wrong window, and I still believe day-one subscription releases are often the wrong move for premium, known-quantity IP. But it is also true that Microsoft is writing real checks and providing real distribution that changes outcomes for a lot of teams.

Phil Spencer said it plainly a couple years ago,

“We’ve put a lot of money into the market, over a billion dollars a year supporting third-party games coming into Game Pass.”

Phil Spencer, CEO, Microsoft Gaming, The Verge, Dec. 1, 2023.

The important part is that this isn’t just indie and AA. There’s an entire top-tier ecosystem that quietly benefits from Game Pass economics too, because for the biggest publishers, these deals can be effectively zero marginal cost money.

Riot is the cleanest example. Riot didn’t need to “port a new game to Xbox” to participate, it partnered on access and benefits across products it already operates at massive scale.

“All Game Pass members will unlock access to… League of Legends (PC): All Champions Unlocked.”

Riot Games, announcement, Riot Games, June 13, 2022.

If you’re Riot, that’s a rare kind of pure margin distribution, you’re monetizing your existing live-service ecosystem by widening the funnel. It’s the same basic logic as Apple getting paid to make Google the default search engine, it costs you almost nothing, and it prints.

EA is another obvious one, and it’s a good example of how Game Pass has evolved into a bundle, not just a library. EA Play, EA’s subscription catalog, is bundled into Game Pass Ultimate, which turns EA’s back catalog into a subscriber acquisition and retention perk for Microsoft, while still generating real value for EA.

“Starting November 10, EA Play will be available on Xbox consoles… as part of Xbox Game Pass Ultimate.”

Xbox Wire, Sept. 29, 2020.

From there it gets even more revealing, because Microsoft isn’t only bundling back catalog, it’s bundling live-service economics. Epic is about as far from “small studio” as you can get, and Fortnite Crew, Fortnite’s paid monthly subscription, is now included as a perk in Game Pass Ultimate.

“Starting November 18, Fortnite Crew becomes part of your Xbox Game Pass Ultimate subscription.”

Xbox Wire, Nov. 14, 2025.

And then Ubisoft. In October 2025, Microsoft explicitly added Ubisoft+ Classics, a curated slice of Ubisoft’s subscription library, into Ultimate alongside Fortnite Crew. At that point, the point is hard to miss, “Ultimate” is increasingly a bundle of bundles, and none of those perks show up for free.

“We’re rolling out our most expansive upgrade yet, including more day one games than ever before, Fortnite Crew & Ubisoft+ Classics for the first time ever…”

Xbox Wire, Oct. 1, 2025.

That’s why this matters. When people talk about Game Pass “subsiding the market,” they sometimes picture only indie day-one deals. The reality is broader. It’s indie, it’s AA, it’s giant publishers, it’s live-service ecosystems, it’s subscriptions bundled into subscriptions, it’s an entire layer of the business that has gotten used to Microsoft being a funding and distribution backstop.

If The Checks Shrink

This is what actually worries me. Whether the AI trade busts or the AI trade booms, Microsoft gets forced into some form of portfolio triage. If the bubble pops, the first response is to protect the core and cut what’s easiest to cut. If the race accelerates and silicon stays tight, the pressure shows up as higher prices and bigger capex, which again forces cuts somewhere else.

In both paths, gaming is exposed, and the ripple isn’t only inside Xbox. If Microsoft starts shrinking Game Pass checks, shrinking marketing support, and shrinking the willingness to fund “reach more players” bets, it hits publishers, it hits AA teams, it hits indie financing, and it hits the parts of the market that quietly benefited from Microsoft acting like a subsidy engine.

That’s the AI risk for games. Not that a prompt generator replaces developers tomorrow. It’s that the economics of the AI arms race, either through collapse or through runaway growth, becomes the catalyst for the next big squeeze in the games business, and I’m increasingly convinced it ends with some form of Xbox separation. At some point, money is money and margin is margin, and Microsoft is going to chase savings and protect the parts of the business that the market rewards most. The economics push you there.

If that day comes, I just hope the transition is smooth for the people inside those orgs. The last thing this industry needs is another brutal snapback, another clawback, another round of “survive the quarter” thinking, twice in the same decade.